Amica Mature Lifestyles Announces Third Quarter Fiscal 2015 Results and Quarterly Dividend

VANCOUVER, BC / ACCESSWIRE / April 10, 2015 / (TSX: ACC) – Amica Mature Lifestyles Inc. (“Amica” or the “Company”) is pleased to announce the Company’s operating and financial results for the three and nine months ended February 28, 2015.

THIRD QUARTER HIGHLIGHTS

- FFO increased 20.8% and diluted FFO per share increased $0.025 per share to $0.144 compared to Q3/14;

- AFFO increased 13.2% and diluted AFFO per share increased $0.015 to $0.126 per share compared to Q3/14;

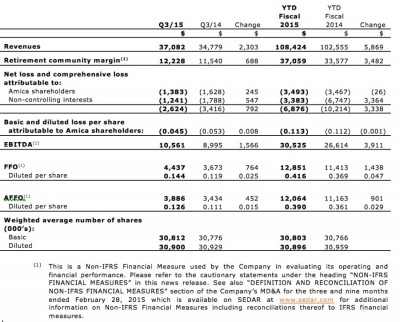

- Revenues increased 6.6% to $37.1 million compared to Q3/14;

- Overall occupancy in mature same communities(1) at February 28, 2015 was 88.9%, compared to 90.1% at May 31, 2014;

- Occupancy in the Company’s community in lease-up at February 28, 2015 was 65.5% compared to 46.9% at May 31, 2014;

- Mature same communities MARPAS increased by 2.4% compared to Q3/14. The Company has experienced monthly year-over-year MARPAS increases in its mature same communities for 62 consecutive months; and,

- The Board approved a Fiscal 2015 fourth quarter dividend of $0.105 per common share.

“The third quarter of Fiscal 2015 built on the momentum generated in the prior two quarters with a 6.6% increase in revenue and a 13.2% or $0.015 per share increase in AFFO diluted per share to $0.126” said Samir Manji, Amica’s Chairman & CEO. “We continue to take advantage of favourable interest rates as we refinance our maturing loans while improving our debt ladder. We remain committed to reducing our due on demand loan balance and strengthening our balance sheet.”

“We experienced a 6.0% growth in our retirement community margin in the third quarter of Fiscal 2015 while realizing occupancy gains of 60 basis points within our mature Ontario communities, as compared to the third quarter last year,” said David Minnett, Amica’s President. “These results, combined with reductions in interest expenses and G&A, illustrate our continued progress towards unlocking the value within our portfolio. We will remain focussed on our margin enhancement initiatives over the next several quarters.”

Financial Highlights

The following table provides operational highlights for the three months ended February 28, 2015 (“Q3/15”) compared to the three months ended February 28, 2014 (“Q2/14”) and the nine months ended February 28, 2015 (“YTD Fiscal 2015”) compared to the nine months ended February 28, 2014 (“YTD Fiscal 2014”):

Consolidated revenues

Q3/15 revenues increased by 6.6% to $37.1 million compared to $34.8 million in Q3/14. YTD Fiscal 2015 revenues increased by 5.7% to $108.4 million compared to $102.6 million in YTD Fiscal 2014. The increase in consolidated revenues is from the increase in retirement communities revenue and other income from the Amica at Kingston co-tenancy.

Retirement communities revenue and expenses

Q3/15 retirement communities revenue increased 4.5% to $36.3 million (Q3/14: $34.8 million), compared with a 3.8% increase in retirement communities expenses to $24.1 million (Q3/14: $23.2 million). YTD Fiscal 2015 retirement community revenues increased by 5.3% to $107.6 million (YTD Fiscal 2014: $102.1 million), compared with a 2.9% increase in retirement community expenses to $70.5 million (YTD Fiscal 2014: $68.5 million).

The following table summarizes the Company’s consolidated retirement communities margin (retirement communities revenues less retirement communities expenses before finance costs and depreciation expense) on a mature community and lease-up community basis for Q3/15 compared to Q3/14:

Consolidated retirement communities margin increased $0.7 million from $11.5 million in Q3/14. The increase is from a $0.2 million increase in mature communities margin and a $0.5 million increase in margin from one lease-up community. The overall, consolidated retirement communities margin percentage increased 0.5% to 33.7% in Q3/15 from 33.2% in Q3/14.

The following table summarizes the Company’s consolidated retirement communities margin on a mature community and lease-up community basis for YTD Fiscal 2015 compared to YTD Fiscal 2014:

Consolidated retirement communities margin increased $3.5 million from $33.6 million in YTD Fiscal 2014. The increase is from a $1.8 million increase in mature communities margin and a $1.7 million increase in margin from one lease-up community. The overall, consolidated retirement communities margin percentage increased 1.6% to 34.5% in YTD Fiscal 2015 from 32.9% in YTD Fiscal 2014.

Other income

Q3/15 other income increased to $0.8 million compared to less than $0.1 million in Q3/14. In Q3/15, $0.7 million of other income was recognized with respect to the settlement of the Amica at Kingston mortgage receivable matter (see “AMICA AT KINGSTON INVESTMENT” below).

_________________

(1)

Comparative information has been updated to reflect communities that have become Mature communities since February 28, 2014 including Amica at Bayview Gardens and Amica at Windsor which became Mature communities in Q1/15 and Amica at Quinte which became a Mature community in Q3/15. Amica at Aspen Woods is now the only community in lease-up.

YTD Fiscal 2015 other income increased to $0.9 million (YTD Fiscal 2014 – $0.4 million) principally due to the interest income and the distributions related to the Amica at Kingston matter.

Finance costs

Interest expense and standby fees decreased by $0.1 million to $4.6 million in Q3/15 and by $0.3 million in YTD Fiscal 2015 to $14.0 million principally due to interest rate reductions achieved on mortgage renewals and refinancing; in YTD Fiscal 2015 these savings were partially offset by an increase in interest expense on the Company’s demand operating loan due to a higher average outstanding loan balance.

In Q3/15, an unrealized loss of $1.4 million was recorded in respect of interest rate swaps on floating rate mortgages compared to an unrealized loss of $0.4 million for Q3/14. For YTD Fiscal 2015, the unrealized loss was $1.5 million compared to an unrealized loss of $0.6 million for YTD Fiscal 2014. The significant movement in the interest rate swap contracts in Q3/15 is attributable to the decline in market interest rates. Assuming the Company holds these mortgages and the interest rate swaps for their full terms, any unrealized gains or losses will reverse and the Company will not realize any gains or losses in respect of these interest rate swaps.

General and administrative (“G&A”) expenses

General and administrative expense increased by 5.4% to $2.7 million in Q3/15 (Q3/14 – $2.6 million) and increased 3.8% to $7.6 million in YTD Fiscal 2015 (YTD Fiscal 2014 – $7.4 million). Included in general and administrative expense are severance and retirement compensation costs of $0.3 million and $0.6 million for Q3/15 and YTD Fiscal 2015 respectively. The severance costs relate to the Fiscal 2015 objective to simplify the organization and were incurred in reorganizing the Company’s corporate functions supporting the retirement communities and include a reduction in personnel. Going forward, the re-organization is anticipated to result in a net annual G&A expense savings of approximately $0.5 million. YTD Fiscal 2015 G&A expenses also include $0.3 million in savings from actual bonus compensation being less than the amount accrued at May 31, 2014.

Depreciation expense

Depreciation expense for Q3/15 increased by 1.1% to $7.5 million compared to Q3/14 and decreased by 0.3% to $22.3 million in YTD Fiscal 2015 compared to YTD Fiscal 2014.

NET LOSS AND COMPREHENSIVE LOSS

For Q3/15, the net loss was $2.6 million compared to $3.4 million in Q3/14. For YTD Fiscal 2015, the net loss was $6.9 million compared to $10.2 million in YTD Fiscal 2014. The decrease in net loss is primarily attributable to improved retirement community margin and the income from the Amica at Kingston settlement of mortgages receivable, these items were partially offset by larger mark-to-market losses on interest rate swaps included in finance costs.

The Q3/15 net loss attributable to Amica shareholders was $1.4 million compared to

$1.6 million in Q3/14. The YTD Fiscal 2015 net loss attributable to Amica shareholders was unchanged at $3.5 million.

EARNINGS BEFORE INTEREST TAXES AND DEPRECIATION (EBITDA)

Q3/15 EBITDA increased by $1.6 million to $10.6 million, compared to $9.0 million in Q3/14. The YTD Fiscal 2015 EBITDA was $30.5 million compared $26.6 million in YTD Fiscal 2014. The primary reasons for the increase in Q3/15 and YTD Fiscal 2015 EBITDA are the increase in retirement communities margin and the income related to the Amica at Kingston settlement of mortgages receivable.

FUNDS FROM OPERATIONS (FFO)

Q3/15 FFO increased 20.8% to $4.4 million ($0.144 per share diluted) compared to $3.7 million in Q3/14 ($0.119 per share diluted). YTD Fiscal 2015 FFO increased 12.6% to $12.9 million ($0.416 per share diluted) compared to $11.4 million in YTD Fiscal 2014 ($0.369 per share diluted). The Amica at Kingston matter contributed $0.6 million to FFO in Q3/15 and YTD Fiscal 2015 (Q3/14 and YTD Fiscal 2014 – $nil).

ADJUSTED FUNDS FROM OPERATIONS (AFFO)

Q3/15 AFFO increased 13.2% to $3.9 million ($0.126 per share diluted) compared to

$3.4 million in Q3/14 ($0.111 per share diluted). Q3/15 maintenance capital expenditures were $0.5 million (Q3/14 – $0.7 million) inclusive of a $0.4 million maintenance reserve (Q3/14 – $0.1 million).

YTD Fiscal 2015 AFFO increased 8.1% to $12.1 million ($0.390 per share diluted) compared to $11.2 million in YTD Fiscal 2014 ($0.361 per share diluted). YTD Fiscal 2015 maintenance capital expenditures were $1.6 million (YTD Fiscal 2014 – $2.0 million) inclusive of a $1.1 million maintenance reserve (YTD Fiscal 2014 – $0.8 million).

The Amica at Kingston matter contributed $0.2 million to AFFO in Q3/15 and YTD Fiscal 2015 (Q3/14 and YTD Fiscal 2014 – $nil).

COMMUNITY UPDATE

Mature same community MARPAS increased by 2.4% for Q3/15 compared to Q3/14 and increased 2.8% for YTD Fiscal 2015 compared to YTD Fiscal 2014. The Company has experienced monthly year-over-year MARPAS increases in its mature same communities for 62 consecutive months. In addition to the ongoing focus on occupancy and ancillary revenue, the continued success on the MARPAS front is the result of the Company wide efforts to raise rents and rates upon turnover, to more accurately reflect the quality of the services provided by Amica.

The following is a summary of occupancy in the Company’s mature same communities:

The extreme and inclement weather over the winter months negatively affected traffic and move-ins of new residents in Ontario, and increasing competitive pressures in some markets resulted in a decrease in occupancy rates. The mature Ontario communities finished Q3/15 at 88.7%, down 0.4% from Q2/15 and up 0.6% from 88.1% at Q3/14. The mature British Columbia communities at Q3/15 were down 2.3% from Q2/15 at 89.4%. The British Columbia occupancy was impacted by softness in two communities which saw higher than usual attrition in the last few quarters and are also facing a very competitive environment. Overall occupancy for mature communities at Q3/15 was down 0.9% from Q2/15. Amica’s marketing teams and community management are focused on increasing traffic with the arrival of Spring. The attention of all management remains on increasing occupancy and extracting value for the services Amica provides and, in conjunction with effective expense control, ensuring those gains flow to the bottom-line in the communities.

The following is a summary of overall occupancy in the Company’s community in lease‑up(1):

- At February 28, 2015, there was one community in lease-up: Amica at Aspen Woods. Amica at Aspen Woods became a lease-up community as of its opening on August 9, 2013.

- Anticipated to increase to 71.7% following an additional 5 net pending move-ins which reflect suites that have been reserved with a deposit made for the reservation, less suites for which notice of termination has been received.

Amica at Aspen Woods, the first community in Calgary, continues to experience improvements in occupancy and remains on track to achieve stabilized occupancy within proforma.

Amica at Kingston Investment

In January 2015, the Company and the Amica at Kingston Co-Tenancy completed the settlement of three mortgages receivable related to the former Amica at Kingston proposed development site. As a result of the settlement of the mortgages receivable, the Company received $1.7 million which includes the repayment of a $0.5 million deposit, $0.2 million in interest income and a $1.0 million distribution from the Amica at Kingston Co-tenancy. As the distribution received was in excess of the Company’s carrying value of the Amica at Kingston investment, the excess distribution of $0.5 million has been recognized as other income for the three and nine months ended February 28, 2015.

The Company also recognized $0.3 million in the share of income from associates for each of the three and nine months ended February 28, 2015 being the Company’s share of the Amica at Kingston Co‑tenancy’s net income for those periods (loss of less than $0.1 million for each of the three and nine months ended February 28, 2014).

The following table summarizes the Amica at Kingston items reflected in the statement of comprehensive loss:

The Amica at Kingston Co-tenancy now has nominal assets and liabilities, and it is intended to wind-up this co-tenancy in the next several months.

Construction Updates and Expansion Projects

Amica at Oakville, in Ontario, which commenced construction (excavation and site servicing) in Q2/13 is expected to open in the summer of 2015. The marketing program has been initiated and reservations are now being accepted.

Upon obtaining construction financing, board approvals and required permits, the Company plans to proceed with the Amica at Swan Lake expansion, as well as the Amica at Dundas expansion. Both the Amica at Swan Lake and Amica at Dundas expansions could commence construction in the next several months.

Acquisition of Additional Ownership Interests in Co-Tenancies

On December 31, 2014, the Company increased its ownership in Amica at Windsor by 0.5% from 49.13% to 49.63%. The aggregate cash consideration was $0.04 million. As the Company controlled the property prior to the acquisition of the additional interest, the non‑controlling interests were adjusted by $0.1 million for the proportion that the Company acquired.

FINANCIAL POSITION

The Company’s consolidated cash and cash equivalents balance, as at February 28, 2015, was $4.9 million compared to $5.3 million at May 31, 2014.

The Company has a $20 million demand operating loan facility secured by a 100% Company owned community. As at February 28, 2015, $10.3 million is available to the Company under this loan facility (amount available is net of $9.0 million drawn on the loan facility and $0.7 million in letters of credit secured by the loan facility). On April 9, 2015, the balance available on the demand loan was approximately $9.4 million.

The Company has obtained proposals for increasing the financing on the demand operating loan facility to $31 million from $20 million. The Company has the option to split the $31 million between a term loan and a new demand operating loan facility. Proceeds of such a financing would be used to repay the existing demand operating loan facility and strengthen the Company’s cash position.

At February 28, 2015, the Company has a working capital deficiency of $244.4 million (May 31, 2014 $261.4 million). This working capital deficiency includes:

In the normal course of business, the Company finances its properties in lease-up using mortgages payable due on demand and regularly has mortgages on other properties that mature within one year of the balance sheet date – these mortgages are reported in the current portion of mortgages payable and contribute $197.9 million to the working capital deficiency at February 28, 2015 (May 31, 2014 – $232.6 million). The Company’s due on demand mortgages payable are primarily on properties that have not achieved stabilized occupancy. The Company monitors their occupancy and income growth for opportunities to seek conventional term mortgage financing to replace the due on demand loans.

One property did not meet the debt service covenant requirements of its mortgage at February 28, 2015. Based on past experience and discussions with the lender, the Company anticipates the loans to continue as if the covenant had been met at February 28, 2015. At February 28, 2015 the outstanding principal of the mortgage is $15.4 million and the full amount has been included in the current portion of mortgages payable. Should the debt service covenant of the mortgage be met in future periods only the loan principal payable in the next twelve months would be included in the current portion of mortgages payable.

The Company anticipates that it will be able to renew or replace all of its mortgages payable as they mature. The following is a summary of the Fiscal 2015 debt maturities refinanced in Q3/15, the remaining maturities in Fiscal 2015 and the maturities in Fiscal 2016:

Re-financed/Renewed in Q3/15

In February 2015, the Company renewed a $21.3 million CMHC insured mortgage which matured on March 1, 2015 for a term of 10 years at a new rate of 2.39% (previously was 3.39%). The renewed mortgage matures on March 1, 2025.

Maturities in Fiscal 2016

The following is a summary of the loan maturities in Fiscal 2016:

- $5.2 million CMHC insured mortgage currently bearing interest at 3.46%;

- $19.5 million non-CMHC insured mortgage currently bearing interest at 4.52%;

- $28.1 million non-CMHC construction loan currently bearing interest on a BA basis at 3.83%;

- $3.0 million non-CMHC loan currently bearing interest at 6%;

- $29.6 million non-CMHC construction loan currently bearing interest on a BA basis at 3.83%;

- $5.0 million non-CMHC loan currently bearing interest at 6%;

- $1.5 million non-CMHC loan currently bearing interest at 6%; and

- $38.3 million non-CMHC construction loan currently bearing interest on a BA basis at 3.51%.

Current 5 and 10 year CMHC insured loan interest rates are approximately 1.7% and 2.4% respectively. Current 5 and 10 year non-CMHC loan interest rates are approximately 3.1% and 3.7% respectively.

CAPITAL EXPENDITURES

In Q3/15, the Company incurred $2.0 million (Q3/14 – $1.2 million) in capital expenditures on its consolidated properties and corporate operations and $0.2 million (Q3/14 – $0.6 million) are classified as maintenance capital expenditures on real estate assets and deducted from FFO in calculating AFFO.

Capital expenditures for consolidated communities and corporate operations for

Fiscal 2015 are budgeted at $5.3 million excluding development properties, of which $2.8 million are maintenance capital expenditures (Amica’s proportionate share of these budgeted maintenance capital expenditures is $2.2 million). Amica is committed to investing in its properties to maintain the high standard it has set in luxury retirement living.

FOURTH Quarter Dividend

The Company’s Board of Directors (the “Board”) has approved a quarterly dividend of $0.105 per common share on all issued and outstanding common shares which will be payable on June 15, 2015, to shareholders of the Company (the “Shareholders”) of record on May 29, 2015.

Results Conference Call

Amica has scheduled a conference call to discuss the results on Friday, April 10, 2015 at 10:00 am Pacific Time (1:00 pm Eastern Time).

To access the call, dial: 1-416-847-6330 (Local/International access)

1-866-530-1553 (Toll-free access)

A slide presentation to accompany management’s comments during the conference call will be available. To view the slides, access Amica’s website at www.amica.ca and click on “Investor Relations” – “Presentations & Webcasts”. Please log on at least 15 minutes before the call commences.

The Company’s unaudited condensed consolidated interim financial statements for the three and nine months ended February 28, 2015 and the management’s discussion and analysis are available on SEDAR at www.sedar.com and available on the Company’s website at www.amica.ca.

Forward-Looking Information

This news release contains “forward-looking information” within the meaning of applicable securities laws (“forward-looking statements”).

These forward-looking statements are made as of the date of this news release and the Company does not intend, and does not assume any obligation, to update these forward-looking statements, except as otherwise required by law. Users of forward-looking statements are cautioned that actual results may vary from forward‑looking statements contained herein. Forward-looking statements include, but are not limited to, statements regarding future occupancy rates; anticipated future revenues, revenue and margin growth/enhancement, financial results and operating performance; unlocking unrealized potential within our existing portfolio; future MARPAS growth; interest rate savings on future re‑financings and mortgage renewals; expectations for interest rate swaps; refinancing due on demand loans and/or maturing mortgages; renewing maturing mortgages; expectations for refinancing the existing demand operating loan to strengthen cash position and re pay the existing loan; the mortgage which did not meet its February 28, 2015 debt covenant will continue as if the covenant had been met; opening Amica at Oakville in summer 2015; Fiscal 2015 capital expenditures excluding development properties of $5.3 million with Amica’s proportionate share of maintenance capital expenditures being $2.2 million; proceeding with the Amica at Swan Lake and Amica at Dundas expansions within the next several months; Aspen Woods achieving stabilized occupancy within proforma; $0.5 million annual G&A savings from recent reorganization; the creation of long term shareholder value; dividends and other similar statements concerning anticipated future events, conditions or results that are not historical facts. In certain cases, forward-looking statements can be identified by the use of words such as “plans”, “expects” or “does not expect”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur” or “be achieved”. While the Company has based these forward-looking statements on its expectations about future events as at the date that such statements were prepared, the statements are not a guarantee of the Company’s future performance and are subject to risks, uncertainties, assumptions and other factors which could cause actual results to differ materially from future results expressed or implied by such forward-looking statements. Such factors and assumptions include, amongst others, the effects of general economic and market conditions; actions by government authorities, including the granting of zoning and other approvals and permits; uncertainties associated with potential legal proceedings and negotiations, including negotiations with respect to construction financing and debt refinancing; and misjudgements in the course of preparing forward-looking statements. In addition, there are known and unknown risk factors which could cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Known risk factors include, among others, risks related to dependence on the ability of Amica’s co-tenancy participants to meet their obligations; interest rate volatility in the marketplace; job actions including strikes and labour stoppages; possible liability under environmental laws and regulations, relating to removal or remediation of hazardous or toxic substances on properties owned or operated by Amica; risks associated with new developments, including cost overruns and start-up losses; the ability of seniors to pay for Amica’s services; regulatory changes; risks inherent in the ownership of real property; operational risks inherent in owning and operating residences; the risks associated with global events such as infectious diseases, extreme weather conditions and natural disasters; the availability of capital to finance growth or refinance debt as it comes due; Amica’s ability to attract seniors with its services and keep pace with changing consumer preferences, as well as those factors discussed in the “Risks and Uncertainties” section of the Company’s Management’s Discussion and Analysis for the three and nine months ended February 28, 2015, and in the “Risk Factors” section of the Company’s Annual Information Form dated August 15, 2014, filed with the Canadian Securities Administrators and available at www.sedar.com. Although the Company has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. There can be no assurance that forward-looking statements, or the material factors or assumptions used to develop such forward looking statements, will prove to be accurate. Accordingly, readers should not place undue reliance on forward-looking statements.

___________________________________

Non-IFRS Financial Measures

This news release makes reference to the following terms: “Earnings Before Interest, Taxes, Depreciation and Amortization” (or “EBITDA”), “Funds From Operations” (or “FFO”), “Adjusted Funds From Operations” (or “AFFO”), “Monthly Average Revenue Per Available Suite” (or “MARPAS”) and “Retirement Communities Margin” (collectively the “Non-IFRS Financial Measures”). These Non-IFRS Financial Measures are not recognized under IFRS and do not have standardized meanings prescribed by IFRS. The Company considers these Non-IFRS Financial Measures relevant in evaluating the operating and financial performance of the Company, along with IFRS measures such as net earnings (loss) and comprehensive income (loss), basic and diluted earnings (loss) per share and cash provided by (used in) operations. Definitions and detailed descriptions of these terms are contained in the MD&A.

- Mature Same Communities: Effective June 1, 2011, mature same communities was defined by the Company to be mature communities that are classified as income-producing properties for thirteen months after the earlier of reaching 90% occupancy or 36 months of operation, with the exception of Amica at Quinte Gardens. Amica at Quinte Gardens will be classified as a mature community thirteen months after the earlier of reaching 90% occupancy or two years post-acquisition by the Company.

About Amica Mature Lifestyles Inc.

Amica Mature Lifestyles Inc., a Vancouver based public company, is a leader in the management, marketing, design, development and ownership of luxury seniors residences. There are 24 Amica Wellness & Vitality(tm) Residences in operation in Ontario, British Columbia and Alberta, Canada. Additionally, Amica has one residence under construction in Oakville, Ontario, one residence in pre-development in Calgary, Alberta and two existing operational residences in Ontario with expansions that are in pre‑development. The common shares of Amica are traded on the Toronto Stock Exchange under the symbol “ACC”. For more information, visit www.amica.ca.

For further information, please contact:

Art Ayres

Chief Financial Officer

Amica Mature Lifestyles Inc.

(604) 630-3473

a.ayres@amica.ca

Troy Shultz

Manager, Investor Communications

Amica Mature Lifestyles Inc.

(604) 639-2171

t.shultz@amica.ca

To view this document as a PDF, go to:

https://www.accesswire.com/uploads/amica04102015.pdf

SOURCE: Amica Mature Lifestyles Inc.

ReleaseID: 427686

Copyright © 1999-2013 SproutNews.com