OCLSW: Compelling Leveraged Upside Potential With A Long Time To Expiry

This Article is Written by Edward Vranic, CFA and Can Also Be Found at His Blog on Seeking Alpha.

REDONDO BEACH, CA / ACCESSWIRE / December 1, 2015 / In my previous articles on Oculus Innovative Sciences, Inc. (NASDAQ: OCLS), I have disclosed that instead of holding the stock, I hold warrants on the stock which trade under the ticker OCLSW. OCLSW was born out of the $6.3 million underwritten public offering from January 2015 and expires five years from that date at a strike price of $1.30.

OCLSW is uniquely positioned as a leveraged security on a volatile microcap health care stock with a lot of upside and has a long time to expiry. Investors who are interested in long-dated call options on equities are often unable find anything with maturities beyond January 2017. OCLSW offers investors another three years on top of that so it really reduces the risk of it expiring worthless because five years is a long time for OCLS to successfully grow into a profitable company. My theory behind owning the warrants is that by 2020 OCLS will have either executed on its business plan and be multiples of its current stock price, or be substantially lower than it is today if it does not. In the downside scenario, both the stock and warrant holders lose substantially all of their capital.

The added bonus beyond the leveraging opportunity with OCLSW is that it trades outstandingly cheap versus the stock. OCLS trades around $1.20 while OCLSW trades around $0.25. If OCLS were to double to $2.40, the warrants would have an intrinsic value of $1.10 ($2.40 less the $1.30 strike price) plus any time value, more than 300% upside. If OCLS was to hit $5, the warrants would have an intrinsic value of $3.70. By owning warrants I can have nearly the same dollar amount of upside potential (the stock price less $1.30 per share plus time value) with much less downside risk because I can invest far less capital for a certain amount of warrants as I would with the same number in stock. A 100,000 position in the stock would cost about $120,000 while a 100,000 position in the warrants would be only about $25,000 invested, assuming one can get the quantity desired at the current market prices.

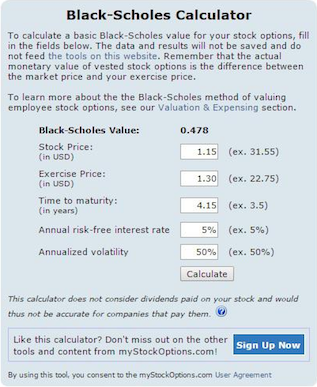

This concept is laid out numerically in the Black-Scholes Option Pricing Model, the most widely used method for calculating the value of derivatives based on the price and volatility of the underlying and the strike price and time to expiry of the derivative. A Black-Scholes option pricing calculator can be used to run various scenarios in attempting to come up with a value for OCLSW:

Using a $1.15 price for OCLS, $1.30 strike price for OCLSW, 4.15 years to maturity (the time between November 2015 and January 2020) and base assumptions of a 5% risk-free interest rate and 50% annualize volatility leads to a fair value of $0.478 for the warrants. If we assumed a risk-free interest rate of 0.1%, the value of the warrants would drop to $0.407.

The assumption most up for debate is OCLS’ volatility. Anacor Pharmaceuticals, Inc. (NASDAQ: ANAC), a large player in the dermatology business, has an implied volatility on its 2017 call options of around 75%:

Using a 75% volatility assumption on OCLS leads to a fair value for the warrants of $0.608:

Using the same implied volatility on OCLS as ANAC likely leads to an understated assumption. ANAC has a market cap over $5 billion while OCLS is 250 times smaller at around $20 million in market cap. A small cap stock is going to have more volatility than a large one, particularly so for a difference of this magnitude. Considering that, I believe that an annualized volatility assumption of at least 100% is warranted.

This leads to a fair value of $0.774 on the warrants. I own the warrants because I strongly believe in OCLS’ ability to capture significant market share in the U.S. dermatology market with its Microcyn-based product line. This is especially so in light of the political pressure on outrageous prices for drugs in the United States as OCLS has very competitive pricing for its dermatology products. However, an investor could also find value in OCLSW simply from a financial engineering perspective even if they had little interest in OCLS as a business. OCLSW make an excellent leveraged speculative play with a long time to expiry.

Disclosure: I am long OCLSW, which are warrants on OCLS expiring in January 2020 at a strike price of $1.30. Owning warrants is within my risk tolerance. Investors should decide if warrants are within their risk tolerance independently of my recommendation. I have been paid for this article. I purchased OCLSW prior to any contact or relationship to the company and this article is an accurate representation of my opinion on OCLS and OCLSW.

Click here to receive future email updates on Oculus Innovative Sciences developments: http://www.tdmfinancial.com/emailassets/ocls/ocls_landing.php.

Disclaimer:

Except for the historical information presented herein, matters discussed in this release contain forward-looking statements that are subject to certain risks and uncertainties that could cause actual results to differ materially from any future results, performance or achievements expressed or implied by such statements. Emerging Growth LLC is not registered with any financial or securities regulatory authority, and does not provide nor claims to provide investment advice or recommendations to readers of this release. Emerging Growth LLC may from time to time have a position in the securities mentioned herein and may increase or decrease such positions without notice. For making specific investment decisions, readers should seek their own advice. Emerging Growth LLC may be compensated for its services in the form of cash-based compensation or equity securities in the companies it writes about, or a combination of the two. For full disclosure please visit: http://secfilings.com/Disclaimer.aspx.

SOURCE: Emerging Growth LLC

ReleaseID: 434225

Copyright © 1999-2013 SproutNews.com